Services

Our progressive thinkers offer services to help create, protect and transform value today, so you have opportunity to thrive tomorrow.

Our services can strengthen your business and stakeholders' confidence. You'll receive professionally verified results and insights that help you grow.

Our tax services help you gain trust and stay ahead, enabling you to manage your tax transparently and ethically.

Our outsourcing services remove the burden and worry of back office processes and reporting requirements across multiple jurisdictions.

Growing demand in energy and resources, plus developments in new forms of energy and investment in sustainability sees significant shifts in these sectors.

Forward-thinking organisations must examine every part of their business to turn the challenges facing the financial services industry into opportunities.

Emerging markets and shifting demand creates new opportunities in food and beverage, we can help you turn these trends to your advantage.

Dynamic businesses need to move with speed and purpose if they want to capitalise on opportunities in hospitality and tourism.

Working with all types of not for profit clients; charities, housing associations, education providers and trade unions, we understand your unique issues.

Our public sector teams provide services tailored to your industry in four key service areas, Operational efficiency, Infrastructure, Governance, and Audit.

Supporting you with pragmatic, tailor-made solutions for improvement and growth, through every stage of the business life cycle.

Whether your goal is to enter new markets, scale operations, manage costs, source funding or comply with regulations, we can help you to succeed.

Tax alert

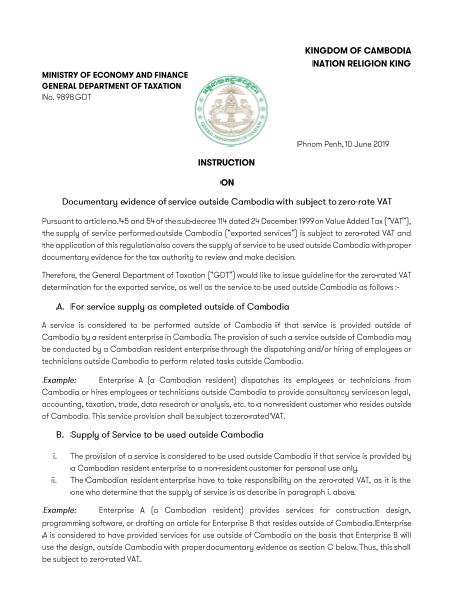

Instruction 9898 on zero-rated VAT on export services

10 Jun 2019The General Department of Taxation (“GDT”) issued Instruction 9898, dated 10 June 2019, which provides further guidelines on when taxpayers may use zero-rate VAT on services performed outside of Cambodia.

The instruction contains discussion on the following:

- When a service is considered to be performed outside of Cambodia. Basically, a service is considered to be performed outside of Cambodia if that service is provided outside of Cambodia by a resident enterprise in Cambodia.

- When a supply of service can be assessed as used outside of Cambodia. Note that the provision of a service is not considered to be used outside of Cambodia if that service is provided by a Cambodian resident enterprise to a non-resident customer for any business objective or economic interest that relates to Cambodia.

- Document evidences needed to support charging zero-rate VAT. Those documents are:

- A contract clearly specifying the service charge, type of services and the place where the services are provided;

- Documents showing payments remitted from outside of Cambodia to a bank in Cambodia for the services;

- Original invoice; and,

- Verifiable accounting records.

Please do not hesitate to get in touch with Grant Thornton Cambodia for any queries regarding this instruction. Our team will be happy to assist you further if required.

See attached copy of Instruction 9898 on zero-rated VAT on export services for further details.